Why Insurance Needs Workbenches, Not Dashboards

Welcome to DX Brief - Insurance, where every week, we interview practitioners and distill industry podcasts and conferences into what you need to know

In today's issue:

Dashboards aren't workbenches: insurance needs to move from insight to action

Why the insurance industry needs a “Human+” model and not full automation

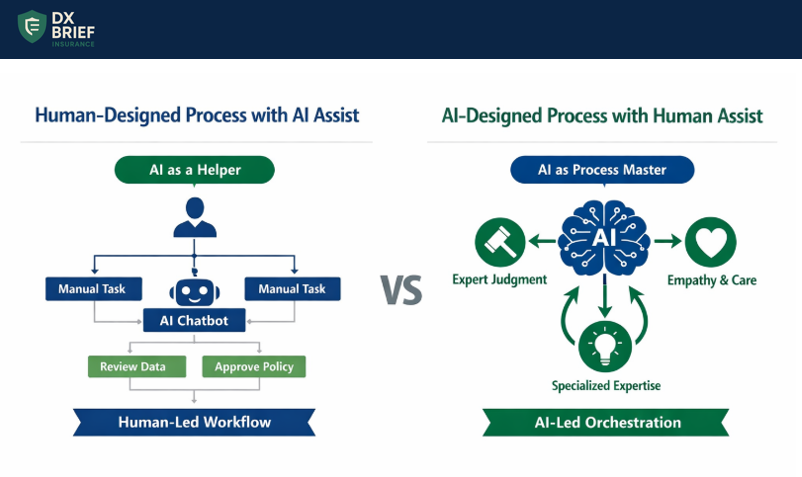

Instead of AI assisting humans through a human-designed process, create an AI-designed process, where humans are called on for judgment and domain expertise

1. Dashboards aren't workbenches: insurance needs to move from insight to action

The Underwriting Intelligence podcast, Insurance in the age of orchestration: Lessons from ServiceNow (Feb 5, 2026)

Background: Nigel Walsh has led insurance transformation at Google Cloud, Capgemini, and Deloitte before taking the Global Head of Insurance role at ServiceNow. His diagnosis of the industry that we've spent 25 years digitizing things layer upon layer, and most of what we call "transformation" is really just dashboarding dressed up as tools. The distinction between a dashboard and a workbench isn't semantic; it's strategic. And the insurance industry's failure to celebrate failure is killing innovation.

TLDR:

A dashboard tells you 73 things you didn't need to know and one thing you did. A workbench puts everything you need at your fingertips to actually do your job, not just observe it.

Insurance has been "layering layers over layers" for 25 years of digitization. If you were redesigning your operations today with a blank sheet of paper, you wouldn't design them this way.

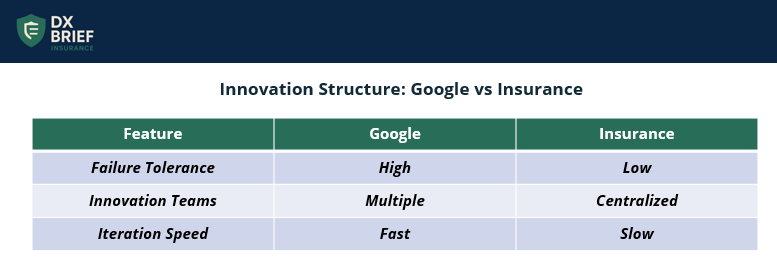

Google's innovation culture succeeds because they have multiple competing teams approaching problems differently and actively celebrate failure. Insurance does neither.

The workbench test: Can you actually do something with it? Walsh uses a simple analogy: think about walking into your garage and picking up your Black & Decker workbench. "Everything is at your fingertips that you need to do, whether it's clamping a piece of wood or your drill's nearby or the screws are there. It's giving you everything that you want in one place to do your job."

This is fundamentally different from a dashboard. "A dashboard is just 'here's the information at your fingertips.' I can't do anything with it, whereas a workbench allows you to then actually do something with it."

We're victims of 25 years of layered digitization. The strategic question is whether you'd build your processes this way if starting fresh. "If you were going to redesign it today with a blank sheet of paper, would you design it this way?" Most transformation leaders inherit systems and optimize incrementally. The better approach is to define what you're actually trying to solve before looking for solutions, and don’t be afraid to explore the “from scratch” option.

Insurance doesn't celebrate failure, and that's killing innovation. Walsh's four years at Google revealed a fundamental cultural difference. At Google, there were Friday sessions where teams would ask: "What have we failed at this week? What can we learn from it?"

The insight isn't that Google is more innovative; it's that they've structured for it. "There's no one right answer. You might have three, five, ten different competing teams in different jurisdictions, a couple of different bets, that all approach innovation in slightly different ways." Insurance companies typically have one innovation team that's supposed to apply innovation to every facet of the organization. That model doesn't work at scale.

Walsh identifies two failure modes: "One is to be so scared of failure that you hide behind your organization that it can't do anything off the rails. Those teams move extraordinarily slowly. The other extreme is where you let anything go, and you're left with an extraordinary mess to tidy up." Finding the middle ground is "a real art form."

What to do about this:

→ Apply the workbench test to every operational tool. For each system your underwriters, claims adjusters, or service teams use, ask: Can they complete their core task without leaving this interface? If not, it's a dashboard, not a workbench.

→ Run a "blank sheet of paper" exercise for one core workflow. Pick your most painful process – new business submission, claims first notice of loss, policy servicing – and design it from scratch without referencing current systems.

→ Create structured space for competing approaches. Instead of one enterprise innovation team, allow 2-3 teams to tackle the same problem with different methodologies. Set a time horizon (90 days), clear success metrics, and let them compete. The variation in approaches often reveals insights that consensus-driven innovation misses.

→ Institute a monthly "failure review" for transformation projects. Document what didn't work, why, and what was learned. Make attendance mandatory for senior leadership. The goal isn't to punish failure; it's to extract learning and signal that experimentation is expected.

2. Why the insurance industry needs a “Human+” model and not full automation

Mighty Finsights podcast, Interview with Joey Bouchard: The Insurance Industry Needed a ‘Human+’ Model (Feb 4, 2026)

Background: Joey Bouchard spent 6 years at Palantir working with a major London insurer before launching QuoteWell. His first attempt was pure tech: automated insurance application ingestion flowing directly to carriers. It nearly killed the company. The pivot? Hiring quality wholesale brokers first, then building technology to supercharge them. The result: a next-gen brokerage with a 2:1 ratio of insurance professionals to engineers.

TLDR:

QuoteWell pivoted from "tech-first automation" to "Human+" (H+): hiring experienced wholesale brokers and building technology that amplifies their capabilities rather than replacing them.

The wholesale brokerage market consolidated dramatically: the top three players went from 30% market share in 2010 to 70% today, creating an opportunity for a differentiated, tech-enabled challenger.

The "Human+" principle changes how you deploy technology. QuoteWell's H+ principle stands for "human-plus," a direct response to the market's question: "Are you a fully automated platform? A comparative rater?"

The answer is emphatic: "Absolutely not. We are driven by people. You could pick up the phone and call us." But there's a critical caveat: "There is a lot of admin that we are trying to automate."

The distinction matters. Brokers and underwriters all have the opportunity to work within the system and see what's going on. The technology is designed for human-to-machine engagement, not human replacement.

Most InsurTech plays position automation as the end goal. QuoteWell positions humans as the end goal, with automation as the enabler. That's a fundamentally different strategic orientation that changes everything from product design to hiring to customer relationships.

You can't bootstrap a relationship business with technology alone. Bouchard admits the early strategy was "trying to be too cute" with automation.

The team attempted to bootstrap the marketplace by automating insurance application ingestion. Essentially giving away software to retail agents as a beachhead into wholesale brokerage. It didn't work. "Within fintech broadly, trying to be too cute or different with your business model too early might be the kiss of death."

The revelation? "We didn't have enough insurance talent on the team. Had we had that from day one, we might have charted a slightly different course."

This is counterintuitive for tech founders who typically believe engineering talent is the constraint. In insurance distribution, domain expertise is the constraint. Technology amplifies that expertise – it can't replace it.

What to do about this:

→ Audit your automation strategy through the "Human+" lens. Ask: Are we building technology to replace human judgment, or to amplify human capability? The former degrades experience while cutting costs. The latter increases revenue while enhancing experience.

→ Evaluate your talent mix ratio. QuoteWell runs 2:1 insurance professionals to engineers. What's your ratio? If you're engineering-heavy in a relationship business, you may be optimizing the wrong constraint.

→ Identify where "too cute" business models are failing. If you're trying to disrupt distribution through pure software, revisit whether the domain expertise constraint is actually being addressed.

3. Instead of AI assisting humans through a human-designed process, create an AI-designed process, where humans are called on for judgment and domain expertise

The Web Talk Show, From Chatbots to Claims Agents: Inside an AI-First Insurance Startup (Feb 3, 2026)

Background: Tuio, Spain's first AI-native insurance company, runs homeowners insurance at 3x the industry profit margin while charging 15-20% less than competitors. They serve the 25-55 age segment that most insurers consider unprofitable. The difference? They didn't bolt AI onto existing processes – they re-engineered their entire operation around it. Here's the framework that made AI their operating system rather than just another tool.

TLDR:

Stop chasing cost-to-serve efficiency. Operating costs are only 10% of your cost base, whereas marketing and claims are 85%, which is where AI decisions can actually move the needle.

Build "next-best-action" agents instead of automation trees. Claims aren't linear, they branch based on coverage, severity, fraud signals, and third parties, which requires AI that handles non-deterministic processes.

Never automate rejections. Keep humans where vulnerability requires empathy, but let AI handle reserve updates, fraud detection, and straightforward approvals automatically.

Efficiency is the wrong target – better decisions are the real prize. Most insurers deploy AI to reduce operating costs. Tuio started the same way with a customer service chatbot in 2023. Then they looked at their cost structure. Operating costs? Only 10% of the business. Marketing and claims combined? 85%.

"Even if you can reduce your operating cost by 50%, you're only getting five percentage points of profit margin. When you're looking at that 85%, if you can improve on that just 10%, you're improving more."

This insight fundamentally changed their approach. Instead of AI for efficiency, they deployed AI for better allocation of that 85%. Growing more efficiently through smarter marketing investment, underwriting smarter with data-driven pricing, and managing claims more effectively (not just more efficiently).

Claims need agents, not decision trees. Traditional automation builds decision trees: if A, then B, then C. But claims don't follow straight lines. They branch based on coverage type, severity, fraud signals, third-party involvement, expert requirements, and repairer networks.

Tuio built what they call "Watson" – a claims agent that processes video evidence, photos, voice notes, customer history, payment patterns, atmospheric data for water damage claims, and even customer navigation patterns. The agent consults manuals on how claims should be treated at each stage, then proposes next-best-actions with confidence levels.

High confidence recommendations like reserve updates get automated. Low confidence items like complex coverage questions get routed to humans. Rejections? Never automated. "When you have to unfortunately reject a claim, the customer is very vulnerable. You want to be humane and empathetic." That's a principle, not a process rule.

Let AI be the process master, with humans as specialized tools. Here's the mindset shift: instead of AI assisting humans through a human-designed process, Watson is the master of the process, and humans are called in as specialized tools when their judgment adds unique value.

This changes hiring, training, and talent allocation. Your people aren't data entry clerks who occasionally make decisions. They're high-value specialists deployed where complex cases and human factors demand expertise. The result? Tuio's AI agent "Leia" achieves 15 points higher NPS than conversations requiring human escalation, and customers leave reviews thanking "Leia" by name.

What to do about this:

→ Audit your cost structure before your AI strategy. Map where your costs actually sit. If you're optimizing the 10% while ignoring the 85%, you're solving the wrong problem.

→ Define your "never automate" principles now. Decide which moments require human empathy – rejections, payment disputes, sensitive coverage questions – before you're tempted to automate them for efficiency.

→ Measure AI by NPS, not just cost savings. Tuio discovered their AI agent outperformed human-assisted conversations on customer satisfaction. Track whether your AI improves experience, not just reduces headcount.

Disclaimer

This newsletter is for informational purposes only and summarizes public sources and podcast discussions at a high level. It is not legal, financial, tax, security, or implementation advice, and it does not endorse any product, vendor, or approach. Insurance environments, laws, and technologies change quickly; details may be incomplete or out of date. Always validate requirements, security, data protection, regulatory compliance, and risk implications for your organization, and consult qualified advisors before making decisions or changes. All trademarks and brands are the property of their respective owners.