Why AI Works at Lemonade, and Breaks Everywhere Else

Welcome to DX Brief - Insurance, where every week, we interview practitioners and distill industry podcasts and conferences into what you need to know

In today's issue:

Lemonade 3x'd revenue while shrinking headcount by building AI into every decision

Why horizontal AI falls flat in insurance

Navigating AI efficiencies when complex insurance products need empathy

1. Lemonade 3x'd revenue while shrinking headcount by building AI into every decision

Farzad podcast: Why AI is about to transform insurance w/ Daniel Schreiber (CEO of Lemonade) (Jan 9, 2025)

Background: Over the past three years, Lemonade has 3x'd revenue, added over a million customers, and grown gross profit 10-fold, while their headcount is smaller than when they started. CEO Daniel Schreiber explains why this isn't a one-time efficiency gain but a structural advantage that compounds: "When ChatGPT 5.1 ticks over to 5.2, did you just become more efficient? For us, the answer is categorically yes. For the rest of the industry, they're just not there and they're not going to be."

TLDR:

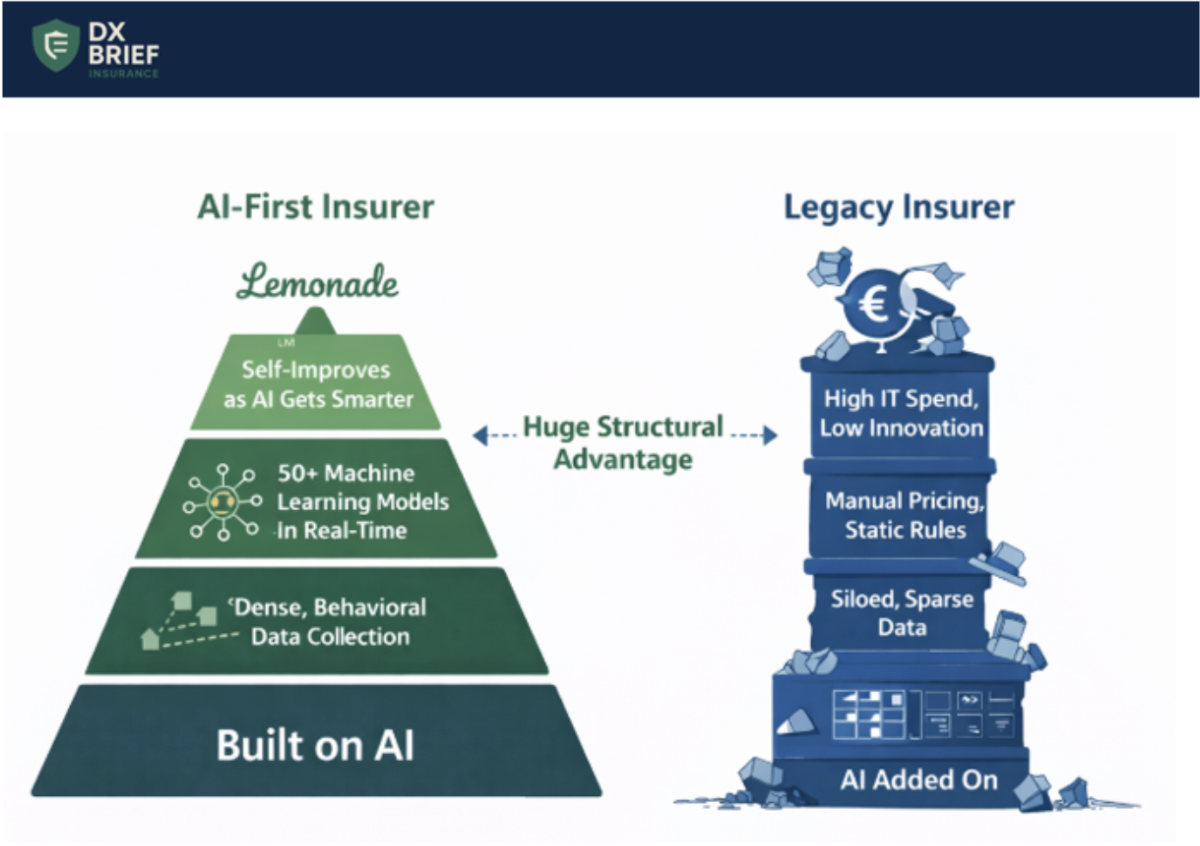

Lemonade captures 100x more data than broker-based interactions and runs 50+ ML models in real time on every customer, enabling them to price based on individual behavior rather than demographic proxies.

Their variable costs have transformed into fixed costs, creating unprecedented operational leverage where growth requires no proportional increase in headcount.

Traditional insurers are structurally handicapped: one major European carrier spends $3 billion annually on IT with "nothing to show for it" – they're maintaining legacy, not innovating.

Being "AI-first" means every improvement in AI makes you better, automatically. Most insurers "sprinkle" AI on existing processes or launch isolated pilots. Lemonade built their entire infrastructure assuming AI would improve exponentially. The difference is structural: when foundation models get smarter, Lemonade's automation indices tick up without any internal project. Schreiber says: "We knew where this was going. We felt that if we built on top of AI, then as the AI gets smarter, we get better."

The practical manifestation is dramatic. When a claim comes in with 30 pages of hand-written veterinary reports, LLMs now process what previously required trained specialists. "We're just finding more and more complicated legal and factual patterns that the LLM can just absolutely crunch and deliver a superior experience at maybe a thousandth or less of the cost." Over 90% of their customer complaints are now about things humans did, not AI.

The data advantage starts at first contact and never stops compounding. Traditional insurance pricing relies on demographic proxies – gender, credit score, neighborhood, education level – because that's all brokers capture. Lemonade's digital interactions generate what Schreiber calls "breadcrumbs" that are "several orders of magnitude" denser. Did the customer search for "cheap insurance" or "good insurance"? Did they hesitate on certain questions? How long did they take?

When you come to Lemonade's website, 50 machine learning models make real-time predictions about you: policy type, churn behavior, claims expectation, cross-sell likelihood. "There is not an insurance company in the world that does this," Schreiber claims. "Frankly, there's very few tech companies that do this real-time, at an initial interaction snapshot."

This data advantage then creates selection advantage. Using telematics, Lemonade prices car insurance on how you actually drive, not how the average male of your age drives. Good drivers see lower rates and stay; riskier drivers find cheaper quotes at Geico (who can't see the difference). "Let that thing turn enough times and you start seeing the power of all this."

Legacy carriers face a "wouldn't start from here" problem that AI acceleration is making worse, not better. Schreiber shares a telling anecdote: Lemonade partnered with a major European insurer expecting to learn from their 200 years of data and 200 data scientists.

Instead, they discovered the company priced renters insurance using a 2x2 lookup table – square footage and age. Why? "The policy needs to be priced by a human being. Sometimes the systems go down and we need to print it out."

The constraint isn't intelligence; it's architecture. Data collection is human (and humans miss signals). Data sits in hundreds of systems that don't talk to each other. There's no modern data lake for AI to study. And the end user is as limited as the beginning. One large carrier confided they spend $3 billion annually on IT as "a black hole, just maintaining things."

Schreiber believes the gap will compound, not close: "If anybody thought the difference between us and traditional insurance is going to shrink because over time they'll catch on… I don't believe that for a second. The differences are going to compound."

What to do about this:

→ Audit your data capture density. Map every customer touchpoint and count the data fields captured versus available. If you're collecting 10-20 fields per interaction while digital natives collect hundreds of behavioral signals, your ML efforts are building on sand.

→ Run the "GPT upgrade test" on your AI initiatives. Ask: If the foundation models we use improve 10x tomorrow, do our results improve automatically? If the answer is "we'd need a new project to take advantage of it," you've sprinkled AI rather than built on AI.

→ Calculate your variable-to-fixed cost ratio. Traditional insurers scale linearly (more customers = more staff). Lemonade demonstrated you can 3x revenue while shrinking headcount. What would your P&L look like with that ratio?

2. Why horizontal AI falls flat in insurance

Applied Systems webinar: Intelligent Insurance Era - How Applied is Investing in AI to Improve the Insurance Industry (Jan 6, 2025)

Background: Applied Systems just processed 40,000 rows of commission reconciliation data in four seconds with 100% accuracy. They're cutting commercial lines submission prep from 5-10 business days to hours. And carriers using their AI-powered risk digitization platform are seeing conversion rates on preferred risk jump nearly 50%. Here's the framework that separates insurance AI that actually works from the chatbots that can't tell the difference between a coverage policy and an HR policy.

TLDR:

Horizontal AI (ChatGPT, general LLMs) struggles with insurance because it doesn't understand account relationships, policy structures, or coverage nuances. It can't even distinguish between "Acme Inc." and "Acme Holdings" as related entities.

The three ingredients for valuable insurance AI: deep industry expertise, access to structured insurance data, and AI engineers who understand the context of insurance workflows.

The goal isn't replacing agents with AI. It's transforming your system of record into a "system of action" that eliminates the 5+ hours per day your staff spends searching for information and the 50-100 emails they manually attach daily.

Divide work into three categories, then attack them differently. The Tidemark framework divides organizational work into "hero work" (winning new business, advising clients, expanding coverage), "administrative work" (reconciling, attaching emails, comparing documents), and "work not done" (policy checking, carrier statement reconciliation – valuable work you outsource to BPOs because you lack capacity). Most insurers throw horizontal AI at hero work and wonder why it underperforms. The leverage is in automating admin work and eliminating work not done entirely.

Why does this matter? Because admin work actively prevents hero work. Your producers and CSRs spend 5+ hours daily just searching for information in your management system. They attach 50-100 emails to activities every single day. That's not a productivity problem; it's a strategic constraint on growth.

Horizontal AI doesn't speak insurance. Ask a general LLM to find "Acme Inc." and it returns Acme Inc., Acme Incorporated, and Acme Holdings without understanding they're related entities. Ask it about a policy and it might return HR policies or company dress codes. Ask it whether liquor liability is covered and it returns "an absolute mess of PDFs for you to manually sift through."

Insurance-specific AI understands account connections (personal lines vs. commercial vs. benefits vs. parent corporations), navigates policy structures (declarations, endorsements, amendments across multiple file types and years), and can trace its logic: "Here's how I reached this conclusion so you can be sure it produced an accurate result."

Data is oil, but it needs refining. Raw insurance data is scattered across PDFs, Excel files, emails, even pictures. Commercial lines submission data spans multiple systems over multiple years. This fragmented data is useless for AI until it's cleaned, enriched, structured, and contextualized. Applied's acquisition of Cytora – a risk digitization platform already showing "product-market fit" with carriers – is designed to transform this chaos into structured data schemas that AI can actually use. The result: submission processing reduced from days to hours, and conversion rates on desired risk up 50%.

What to do about this:

→ Audit your admin work burden this week. Track how many hours your team spends searching for information, attaching emails, and reconciling statements. If you're like most agencies, you'll find 15+ hours per week per accounting staff member on reconciliation alone. That's your AI investment case.

→ Test vertical vs. horizontal AI on a real coverage question. Take a complex coverage inquiry (does this policy include liquor liability?) and run it through both your general AI tools and any insurance-specific solutions. Document which one can trace its reasoning through declarations, endorsements, and exclusions.

→ Map your "work not done" to potential AI solutions. Identify the valuable work you're outsourcing to BPOs or simply not doing. Commission reconciliation, policy checking, and policy comparisons are prime candidates for AI automation with measurable ROI.

3. Navigating AI efficiencies when complex insurance products need empathy

Insurtech Insights Webinar by CAPCO - A Human Touch: Harmonising Digital Distribution & Personal Connection (Jan 9, 2026)

The headline: Nearly 40% of insurance customers worry about losing human support in critical moments. Prudential Hong Kong has committed to becoming "an AI-first insurer with human touch." Fi Life built triggers that automatically switch from chatbot to human agent the moment someone mentions "claim" or "death." And American Family Insurance is using Gemini to prepare agents before calls, support them during conversations, summarize afterward, and analyze sentiment, without replacing a single human interaction.

TLDR:

The one skill AI must never touch is empathy, particularly in claims, crisis moments, and complex life decisions. Fi Life's chatbot immediately transfers to humans when certain trigger words appear. As one panelist put it: "The beauty of human beings is we are perfectly imperfect, and that's how you build trust."

Simple products (travel, motor) work as fully digital journeys. Complex products (life insurance, wealth planning) require human guidance because they involve taxation, regulation, and emotional decisions.

The biggest barrier to AI adoption isn't technology, it's back-end process. Prudential discovered "it's actually the process, not the technology itself" blocking their AI implementations.

Design for emotional triggers, not product categories. Insurance buying is driven by emotion – the amygdala, not spreadsheets. People buy after hearing a story, sharing an experience, or facing a life event that triggers fear or love for family.

Google Hong Kong sees this in search data: queries have shifted from "compare best term life insurance" to "how can I best transfer money and leave money to my kids if anything happens to me." That's not a data point. It's anxiety, love, and fear.

Most insurers design digital journeys around product complexity. Better insurers design around emotional state. Simple administrative questions (when is my payment due?) can be handled by AI. But the moment someone mentions death, claim, or crisis, human empathy must be available immediately, not after a menu tree.

Use AI to enhance the conversation, not replace it. American Family Insurance has deployed Gemini across the entire agent workflow: preparing agents with policy holder context before calls, providing real-time guidance during conversations, summarizing discussions afterward, and analyzing call sentiment for continuous improvement. The result isn't fewer human interactions, it's better ones.

Capco is experimenting with speech-to-text that listens to agent-client conversations and automatically completes forms, flags missing KYC requirements, assesses affordability, evaluates product suitability, and prompts agents when they've missed something. The conversation stays human. The paperwork becomes invisible.

Fix your backend before you deploy AI. Ivan Choy at Prudential Hong Kong said: "Oftentimes it's the backend process that's hindering us, and not the technology itself." Legacy systems, disconnected data, and undefined data governance create bottlenecks that no AI can solve.

Prudential has been in Hong Kong for 60 years. They've launched countless products. Now an agent trying to answer "is this disease covered in my policy?" faces a knowledge management nightmare.

The foundation work isn't glamorous: data strategy, data cleansing, golden source of truth. But without it, AI projects stall. Capco's data practice has doubled each year for three years running because insurers finally recognize they can't run AI on fragmented data.

What to do about this:

→ Build explicit human-handoff triggers into every AI touchpoint. Identify the words and topics (death, claim, cancer, crisis) that should immediately route to human agents. Test your chatbots and voice systems to ensure these triggers work instantly.

→ Pilot AI that enhances agents, not replaces them. Start with one use case: pre-call preparation, real-time conversation support, or post-call summarization. Measure whether agents feel more confident and whether customers report better experiences.

→ Audit your backend processes before your next AI initiative. Map the end-to-end workflow for one key customer journey. Identify where fragmented data, manual handoffs, or undefined processes will block AI implementation regardless of how good the technology is.

Disclaimer

This newsletter is for informational purposes only and summarizes public sources and podcast discussions at a high level. It is not legal, financial, tax, security, or implementation advice, and it does not endorse any product, vendor, or approach. Insurance environments, laws, and technologies change quickly; details may be incomplete or out of date. Always validate requirements, security, data protection, regulatory compliance, and risk implications for your organization, and consult qualified advisors before making decisions or changes. All trademarks and brands are the property of their respective owners.