Human-Led, Agent-Operated: The Frontier Firm Blueprint

Welcome to DX Brief - Insurance, where every week, we interview practitioners and distill industry podcasts and conferences into what you need to know.

In today's issue:

Frontier insurance firms are operating "human-led, agent-operated" playbooks

Build competencies, buy commodities: Ledgebrook cut quote turnaround time from weeks to minutes by building core systems and buying everything else

The smartest carriers are hiring hundreds of AI engineers for previously off-limits functions like underwriting and risk selection to rethink operations from the ground up

1. Frontier insurance firms are operating "human-led, agent-operated" playbooks

Scouting for Growth podcast w/ Sabine VanderLinden, The Frontier Firm Playbook: How Leaders Are Building Agentic Enterprises at Scale (Feb 12, 2026)

TLDR:

The Frontier Firm is "human-led, agent-operated" – Microsoft's framework describes organizations where humans set strategy and AI agents execute entire workflows autonomously, with humans intervening only for exceptions.

The "Agentic Five" insurance companies have chosen 3 distinct paths: Ping An built a complete tech ecosystem from within (21,000 developers, 3,000 AI scientists). Aviva launched an industry-first AI memorization tool after 18 months of rigorous testing. And Chubb became a platform ecosystem architect.

The five levers that separate leaders from laggards: data governance, ecosystem partnerships, change management, AI integration, and leadership alignment. Most fail at lever three – cultural transformation.

The three phases of human-AI collaboration. Microsoft's framework describes a clear evolution.

Phase One: AI assists humans with specific tasks (you prompt, you get an answer).

Phase Two: AI agents join teams as digital co-workers, handling discrete tasks under human guidance.

Phase Three: autonomous agents execute entire workflows with humans setting strategy and intervening only for exceptions.

Most insurers are stuck in Phase One. The Agentic Five are operating in Phase Three.

The Agentic Five chose distinct strategic paths.

Ping An built from within. It handles 1.5 billion customer inquiries through AI agents annually. Their claims processing ends in 7.4 minutes, sometimes seconds. 93% of their underwriting is done autonomously. They've incubated 11 independent technology affiliates with a combined valuation exceeding $70 billion. They chose to build a complete technology powerhouse ecosystem from within. As Sabine puts it: "They are a tech giant that happens to sell insurance."

Allianz perfected the venture client model through Allianz X – they don't just invest in startups, they become early customers to rapidly integrate new technology, combining equity, reinsurance capacity, and operational partnerships. They manage a portfolio of 25 companies with approximately $2 billion in assets under management.

Chubb chose the platform ecosystem architect path. Chubb Studio built the rails on which the future of insurance distribution will run. Their AI optimization engine provides AI-as-a-service to digital partners. Rather than competing with digital platforms, they enable them.

Zurich exemplifies the governance-first approach: hiring a Chief AI Officer, opening a dedicated AI research lab, ensuring AI is deployed responsibly at scale.

Aviva proved you can build trust and achieve competitive advantage simultaneously by rigorously testing their AI memorization tool for 18 months before launch.

The five levers, and where most fail. Sabine identifies five critical levers:

data governance and ethics,

ecosystem partnership,

transformational change management,

AI integration, and

leadership alignment.

The bottleneck that separates Phase Two from Phase Three organizations? Lever three – cultural transformation.

"You can have the best technology in the world, but if your people don't embrace it, your transformation will fail." Even Zurich, a member of Microsoft's Frontier Firm cohort, admits to ongoing challenges driving enterprise-wide cultural change. This requires empathy, communication, and a commitment to bring your people along. It requires change champions in-house. It requires heavy investment in upskilling. AI academies aren't optional – they're foundational.

What to do about this:

→ Identify one high-impact, data-rich workflow and redesign it around human-AI partnership. The Aviva model: focus on underwriting or claims, deploy an AI agent that handles data synthesis, let humans focus on judgment. Give a cross-functional "fusion team" a 90-day mandate to deploy.

→ Decide your strategic path: build, partner, or platform. Ping An built from within, but they have 21,000 developers. Allianz partners deeply through venture client models. Chubb became infrastructure. Be honest about your capabilities and choose accordingly.

→ Invest in change management as seriously as technology. The cultural piece is often the most challenging, and the lever where most organizations fail. Create AI academies, appoint change champions, communicate relentlessly. This is a leadership challenge above all.

2. Build competencies, buy commodities: Ledgebrook cut quote turnaround time from weeks to minutes by building core systems and buying everything else

The Pair Program, Insurtech at Speed: Engineering the Future of Specialty Insurance w/ Nathan Hall, CTO at Ledgebrook, and Mike Mansell, principal at American Family Ventures (Feb 10, 2026)

Background: Ledgebrook, a fast-growing Excess & Surplus (E&S) commercial insurer, reduced quote turnaround time from weeks to minutes, and they're winning business on speed and service, not price. CTO Nathan Hall built the entire technology stack around one principle: build anything that's core competency, buy everything else. Here's how they architected for speed and why they're hiring engineers from fintech and healthtech, not insurance.

TLDR:

Speed beats price in specialty insurance: Ledgebrook wins by responding in minutes while competitors take weeks. Brokers remember who responds, not who's cheapest.

Build core competencies, buy commodities: Ledgebrook built their own quoting and rating engine but purchased their policy administration system. Know the difference.

AI automates workflows, humans make decisions: a chatbot handles rating, appetite checks, and data extraction, cutting clearance from 60 minutes to 3 minutes. But reinsurance partners won't accept AI making underwriting decisions, so humans remain in the loop.

Meet brokers where they are – don't try to change their behavior. Ledgebrook's most counterintuitive decision? They built their entire intake system around email. Not a digital portal, not an API-first submission flow, email. Why? Because that's how wholesale brokers already work. "It's really hard to convince brokers who are very used to just searching for the name of the person they remember and forwarding the email on," Nathan explains.

Other InsurTechs built elaborate digital portals that brokers won't use. Ledgebrook built AI that extracts data from emails, clears submissions, and generates preliminary quotes – all without forcing behavioral change. The lesson: automation should absorb friction, not relocate it.

Build core competencies, buy commodities. Nathan's philosophy is: "Build anything that's part of your core competency." For Ledgebrook, that's speed and underwriter efficiency, so they built their own rating engine and clearance automation.

Policy administration (tracking policies post-issue, handling endorsements) wasn't a differentiator, so they bought a system with a well-defined data model and rich API ecosystem to build on top of.

Too many transformation leaders treat every system as equally strategic. They're not. The systems that make you faster or smarter than competitors deserve custom development. The systems that just need to work should be purchased. Ledgebrook's 35-person engineering team stays focused because leadership made this distinction early.

AI augments humans, and reinsurers demand it stays that way. Ledgebrook's AI chatbot handles the grunt work: extracting data from emails, checking underwriting guidelines, rating submissions, and returning preliminary quotes. This cut clearance time from 60 minutes to 3 minutes. But here's the guardrail: reinsurance partners explicitly do not want AI making binding decisions. "They naturally can be a little more risk-averse, and having [AI make decisions] just doesn't really align."

This isn't a bug, it's a feature. The broker relationship is human. The underwriting judgment is human. AI handles the data synthesis so humans can spend time on what actually matters: building relationships and making decisions. A VP from a billion-dollar-premium carrier watched Nathan generate a quote with one button click and asked him to do it again, because at his previous company that process took two days through the IT department.

Hire builders who've seen good, not people who know insurance. Ledgebrook's engineering team comes from fintech, healthtech, and other regulated industries – not insurance. Why? They've seen what good looks like. Insurance veterans know how things have always been done. Engineers from modern tech companies know what's possible. Pair them with business-side hires who have deep insurance experience (who "know what bad is"), and you get a team that can actually reimagine processes.

The culture test: Is your engineering team curious enough to take actuarial classes voluntarily? American Family Ventures' Mike Mancel noticed that Ledgebrook engineers – none from insurance backgrounds – were pursuing actuarial designations on their own. That's the builder's mindset.

What to do about this:

→ Map your value chain and classify each system: core vs. commodity. Be ruthless. If a system doesn't make you faster, smarter, or more accurate than competitors, it's a candidate for buy, not build. Redirect engineering resources to true differentiators.

→ Talk to brokers about response time, not just price. Ledgebrook's insight came from direct broker feedback: "A lot of times we'll send it out and we won't hear back for four weeks and it was due three weeks ago." If your brokers are saying similar things, speed is a bigger lever than you think.

→ Hire for builder's mindset over domain expertise. For engineering roles, prioritize candidates from modern tech environments who've built in regulated spaces (fintech, healthtech, defense). Pair them with domain experts who can translate business needs. The combination is more powerful than either alone.

3. The smartest carriers are hiring hundreds of AI engineers for previously off-limits functions like underwriting and risk selection to rethink operations from the ground up

The Future of Insurance podcast: Solving Real Problems in the Era of Intelligent Insurance w/ Tony Lew (Feb 10, 2026)

Background: After a decade of hype cycles – from "InsurTech will replace carriers" to "Lemonade will dominate" – the insurance innovation landscape has finally matured. Tony Lew, co-founder of InsureTech New York and an active investor since 2022, reveals why the smartest carriers are now hiring hundreds of AI engineers for previously off-limits functions like underwriting and risk selection, and why simply layering AI on legacy processes is the fastest way to fall behind competitors who are rethinking operations from the ground up.

TLDR:

The "tourist money" has left InsurTech, leaving founders who actually understand insurance and are solving real problems. This is the best time to find technology partners with genuine domain expertise.

Major carriers like AIG and Chubb are building internal AI capabilities for underwriting and risk selection – areas they previously kept closed to vendors – signaling a fundamental shift in how core insurance decisions will be made.

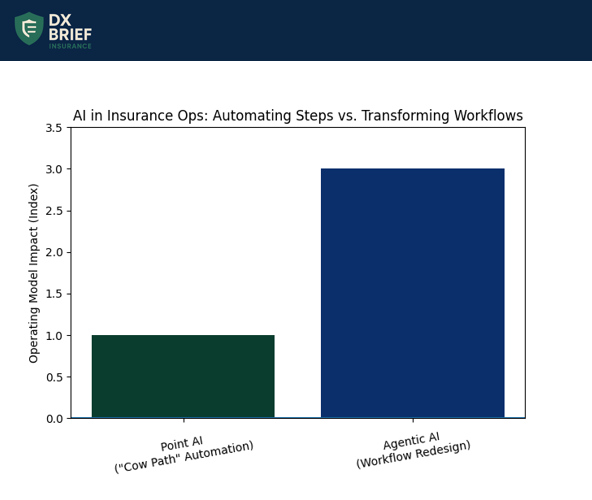

Applying AI to existing legacy processes is "paving the cow path" (= automates inefficient processes). The real opportunity is rethinking whether those processes should exist at all.

Vertical knowledge is the moat, not the technology itself. Lew shares a critical insight from an OpenAI executive responsible for startup partnerships: "He said he would invest in companies who have vertical knowledge and are able to apply that knowledge and leverage OpenAI technology." This is precisely what InsurTech founders with deep industry experience can deliver.

OpenAI might achieve 60% accuracy extracting data from loss runs, but someone with insurance knowledge can "tweak it, make it really good." The implication for digital transformation leaders: don't outsource your AI strategy to general-purpose tech vendors. Partner with those who understand insurance workflows, regulatory constraints, and the nuances of risk selection.

One-off AI capabilities won't move your combined ratio. Many carriers are implementing AI in isolated pockets: a chatbot here, a document extraction tool there. But these point solutions don't address full operating model transformation.

The real opportunity lies in agentic AI that automates entire workflows. "Insurance is so workflow dependent. There's so many steps in everything and AI can actually automate a lot of those things."

When a customer service email arrives, agentic AI can categorize the question, start different workflows, and take action, with or without human intervention. That's the difference between shaving costs and fundamentally changing your expense ratio.

The "zombie" risk is real, and AI makes it worse. There’s a growing category of "InsurTech zombies": PE-backed companies that can't invest in R&D, VC-funded startups that burned through capital, and founder-owned firms without resources for AI talent.

These companies have good technology but can't keep pace with carriers investing heavily in AI capabilities. "Those that are investing in it are going to get so competitive that it's going to change the dynamics of who's going to be really leading."

The gap between AI-enabled and AI-absent players is about to widen dramatically. If your technology partners aren't investing in AI, they're holding you back.

The one-person AI agency is emerging. Lew has seen two companies in recent weeks generating close to a million in premium with essentially one person running AI-based distribution. "Basically an AI-based agency... just been out for a few months."

This isn't theoretical – it's happening now. The implication: distribution economics are about to shift dramatically, and the winners will be those who figure out how to leverage AI for growth, underwriting, and claims simultaneously.

What to do about this:

→ Audit your AI investments for "cow path paving." List every AI initiative in progress. For each, ask: "Are we automating an existing process, or are we questioning whether this process should exist at all?" Kill or reshape projects that merely digitize legacy workflows.

→ Evaluate your technology vendors' AI roadmaps. Request specifics on their AI investments: headcount, LLM strategy, agentic workflow capabilities. If they're not actively building, they may become zombies that hold you back.

→ Pilot agentic AI in one high-volume workflow. Select a process with significant manual steps (claims triage, policy servicing requests, underwriting documentation). Implement an agentic solution that can categorize, route, and take action – not just extract information.

Disclaimer

This newsletter is for informational purposes only and summarizes public sources and podcast discussions at a high level. It is not legal, financial, tax, security, or implementation advice, and it does not endorse any product, vendor, or approach. Insurance environments, laws, and technologies change quickly; details may be incomplete or out of date. Always validate requirements, security, data protection, regulatory compliance, and risk implications for your organization, and consult qualified advisors before making decisions or changes. All trademarks and brands are the property of their respective owners.